What’s Next for FedNow?

10 real-time payment predictions

Welcome back.

In July, the US government finally launched its FedNow real-time payments (RTP) infrastructure, posing new challenges and opportunities for payments players across the F-Prime Fintech Index. In this month’s edition of Fintech Prime Time, Rocio Wu draws on her knowledge of the international payments landscape to make 10 predictions about the development of instant payments in the US. As we’ll see, several of the largest payments companies in the F-Prime Fintech Index — including Shopify, PayPal, and Adyen — are already deeply involved in the delivery of instant payment rails to American users.

Meanwhile: Payments companies in the F-Prime Fintech Index are up more than 100 percent over the last 12 months, outperforming NASDAQ (~31 percent), the Emerging Cloud Index (~23 percent), and even the broader F-Prime Fintech Index (~89 percen) over the same time period.

The RTP Gold Rush: 10 FedNow Predictions

By Rocio Wu

The United States’ long-awaited real-time payments (RTP) system, FedNow, launched in July. The availability of instant money transfers has huge potential to impact virtually all players in the economy, from financial institutions and corporate giants to online shoppers, small business owners, and employees.

We in the US are late to the RTP game, and can learn a lot from other countries’ experiences. However, the US has a uniquely fragmented banking landscape, with plenty of other payment methods currently dominating American payments. So how will the FedNow launch affect the space? Which use cases will gain the most traction? How are financial institutions and startup disruptors rising to the occasion and filling in those critical gaps? Where do the economic opportunities lie?

Luckily, we have a time machine that lets us reference the evolutions of RTP adoption in other markets and make predictions about our own future. Here are ten predictions that flow from the launch of FedNow.

1. FedNow will start a domino effect of RTP adoption, led by consumer led cases

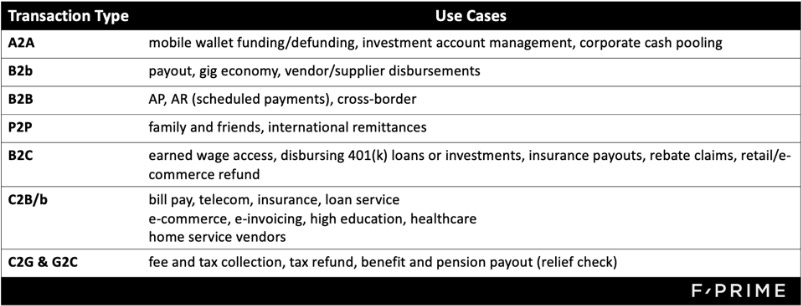

Detail: Tools like Venmo, PayPal, and Zelle have led many to believe that peer-to-peer (P2P) payments have been solved, and FedNow therefore poses a bigger opportunity in the B2B payments space. However, The Clearing House (TCH) reports that the majority of transactions on its RTP product are still driven by consumer use cases.

Signals: This adoption pattern is consistent with the evolution of Brazil’s Pix system, where P2P payments accounted for 80 percent of transactions immediately following its launch. That figure has since declined to 67 percent as person-to-business transactions accelerate — today, 20 percent of Pix transactions are P2B payments.

2) Mass network connectivity could take close to a decade

Detail: The last time US banks embraced ubiquitous electronic payment rails was the launch of the automated clearing house (ACH) network for direct deposits in the 1970s — and it took between seven and 10 years. Incumbents and startups are racing to get the banks onto FedNow rails, but it will be a long road given the fragmented American banking landscape.

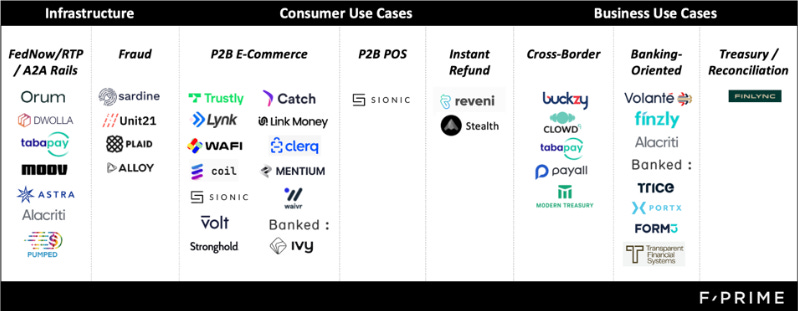

Signals: Organizations like J.P. Morgan, Wells Fargo, and Adyen are among more than 300 financial institutions using FedNow as of December. We estimate that group will swell to 1,000 in 2024 as banks learn about fraud prevention, liquidity management, and other factors. Remember: the US has almost 8,000 banks and credit unions.

3) FedNow will replace cash and checks, but not credit cards

Detail: For now, a lot of B2B transactions still occur via checks (21 percent of payment value), but we predict that number will decline with the launch of FedNow. Meanwhile, the 2020 acceleration away from cash to credit cards has continued into 2023. Cash use declined from 31 percent to 18 percent of all payments between 2016 and 2023, and credit card usage increased at the exact same rate. Overall, we believe that FedNow-enabled RTP will accelerate cash’s demise in the US, especially among younger demographics.

Signals: The rate and reasons for cash’s decline vary by country, and the path is not always linear. The UK’s RTP system, named Faster Payments, replaced cash and checks over time while credit card usage remained consistent. In India, the growth of its account-to-account (A2A) real-time payments system, called UPI, is the primary driver for cash’s decline, whereas digital wallets have claimed cash’s mantle in Saudi Arabia and Vietnam.

4) P2B account-to-account use cases will grow slowly, but steadily

Detail: Merchants are drawn to account-to-account (A2A) payments because they’re cheaper than credit cards and the money arrives instantly. While American banking fragmentation and credit card ubiquity will drag merchants’ adoption of A2A payments, some local retailers are encouraging customers to try an A2A/ACH solution called Pay by Bank as a cheaper and faster alternative to credit cards. Adoption will accelerate once chargebacks on A2A transactions and dispute management becomes available.

Signals: The P2B use case for A2A payments tends to succeed in markets where banks take the lead. In Poland, for example, the BLIK A2A mobile payment solution is a cooperative effort between six major banks, supported by banking apps, e-commerce storefronts, points-of-sale, P2P payments, cash deposit systems, and ATM withdrawals. BLIK now claims 67 percent of Polish e-commerce payments. A similar system in the Netherlands, called iDeal, accounted for 62 percent of Dutch e-commerce transactions in 2022.

5) FedNow will serve as an incremental improvement on US payment infrastructure, not a paradigm shift

Detail: Very few great companies were built off of RTP innovation around the world. However, many have leveraged RTP to expand their product accessibility and functionality.

Signals: Pix fueled the rise of digital wallets like PicPay, which doubled its digital wallet share of POS transaction value from eight percent in 2021 to 15 percent a year later. Pix is free to consumers, so credit is PicPay’s main monetization channel. Meanwhile, Nubank leveraged Pix to accelerate account funding and reach customers who didn’t have a bank account. In the US, B2B payments companies like Melio and Adyen have already added FedNow rails to their product menu.

6) If there’s going to be a QR code renaissance, interoperability is a prerequisite

Detail: QR codes are a ubiquitous payment method in Asia and parts of Latin America — they currently initiate nearly 20 percent of Pix transactions — but interoperability is key to their success. In other words: a code must be scannable no matter which bank issued it or which payment app is scanning it.

Signals: Visa recently launched its Visa+ product to power interoperable payments across P2P apps. It currently supports PayPal and Venmo, and will soon incorporate Western Union, TabaPay, i2c, and DailyPay. Visa is playing the long game on RTP, with a plan to become the new rails — and even an identity layer with their unique payment handle — that will consolidate the fragmented P2P landscape and hedge against the risk of credit cards losing share to A2A.

7) Digital wallets will become the next battlefield in e-commerce and at the point of sale

Detail: Digital wallets recently became the leading online payment method in the US, with 32 percent market share in 2022 — a figure that has more than doubled since 2014. The American credit and debit card markets are increasingly intermediated by a handful of major digital wallet brands: PayPal, Google Pay, and Apple Pay, plus a handful of challengers. As FedNow rolls out, we believe A2A will surpass debit and credit cards as the main source of digital wallet funding, intensifying the battle for the “top of the wallet.”

Signals: In terms of digital wallet adoption, China sets the pace. A remarkable 81 percent of e-commerce transaction value occurs through digital wallets there, far exceeding India, which has the second-highest market adoption at 50 percent. At the PoS, Chinese digital wallets accounted for 56 percent of transaction value. In India, the figure was 35 percent.

8) Authorized push payment fraud will rise, requiring dual responses from the public and private sectors

Detail: In the age of generative AI, authorized push payment (APP) fraud is going to be even harder to mitigate. While it remains unclear how FedNow plans to protect consumers from APP fraud on a public policy level, real-time payment provider Zelle recently bowed to regulatory pressure and agreed to indemnify users who fell victim to imposter scams. More fintech startups are assembling competing data consortiums that would prevent the use of compromised identity information to defraud multiple apps and services.

Signals: In the UK, the vast majority of APP fraud cases start online, prompting the payments regulator to step in with scam reimbursement. In Brazil, however, Pix-related financial crime was a predominantly offline phenomenon, prompting the Central Bank to limit transfers at night amid a kidnapping spree. On the private side, Nubank has implemented a system that places lower transfer limits on money that is sent via a telecom or public WiFi, as opposed to a home WiFi network. And PicPay was the first to launch Digital Wallet insurance to offer protection from identity theft and scams.

9) Consumers and small businesses are willing to adopt faster, cheaper payments

Detail: We believe that these two groups stand to gain the most from real-time payments infrastructure. Consumer use cases include account funding and defunding for digital wallets, neobank accounts and investment accounts, and instant pay access for gig economy workers. Meanwhile, under the payments status quo small businesses are currently stuck choosing between speed (via a credit card and its 2.9 percent fee) and price (a slower ACH bank transfer) — FedNow gives them a third option. Overall, we see FedNow driving efficiency in payment services and, more importantly, stimulating competition among existing payments and financial service providers rather than creating brand new categories.

Signals: In Q2 of 2022, instant payroll accounted for 15 percent of the total payment volume on TCH’s RTP system, growing 104 percent over the prior quarter. Big retailers like Walmart have also expressed their interest, as more than 45 percent of calls to its call centers boil down to, “Where is my refund?”

On the B2B front, Shopify announced a partnership with invoice payments platform Melio to offer direct bill payments services, including an option to pay through a bank account. This will improve Shopify merchants’ experience by shortening their cash conversion cycle and reducing their working capital needs.

10) FedNow will fuel cross-border money movement

Detail: Last year The Clearing House, EBA Clearing and SWIFT announced an immediate cross-border payments pilot. In theory, the US might connect FedNow with other RTP systems to facilitate instant clearing for multiple currencies, international remittances and even global transaction banking.

Signals: Integration between Thailand’s PromptPay, Singapore’s PayNow, Malaysia’s DuitNow, and India’s UPI real-time payment systems has stimulated increased cross-border money movement. In Scandinavia, the P27 cross-border A2A payment system combines eight payment clearing systems into one integrated real-time, instant-clearing, multi-currency payment platform. And Indians living in 10 countries (including the US and UK) will soon be able to use UPI, paving the way for a global remittance network.

This story was originally published on Forbes.