Wealth & Asset Management: From Underdog to Market Driver?

Plus: New Fintech Index listings coming soon

Welcome back to Fintech Prime Time, with data and analysis based on the F-Prime Fintech Index. This month, a series of soon-to-be new additions to the Index and the Q2 performance metrics have us zooming in on one subsector: wealth and asset management (WAM).

The WAM Rally

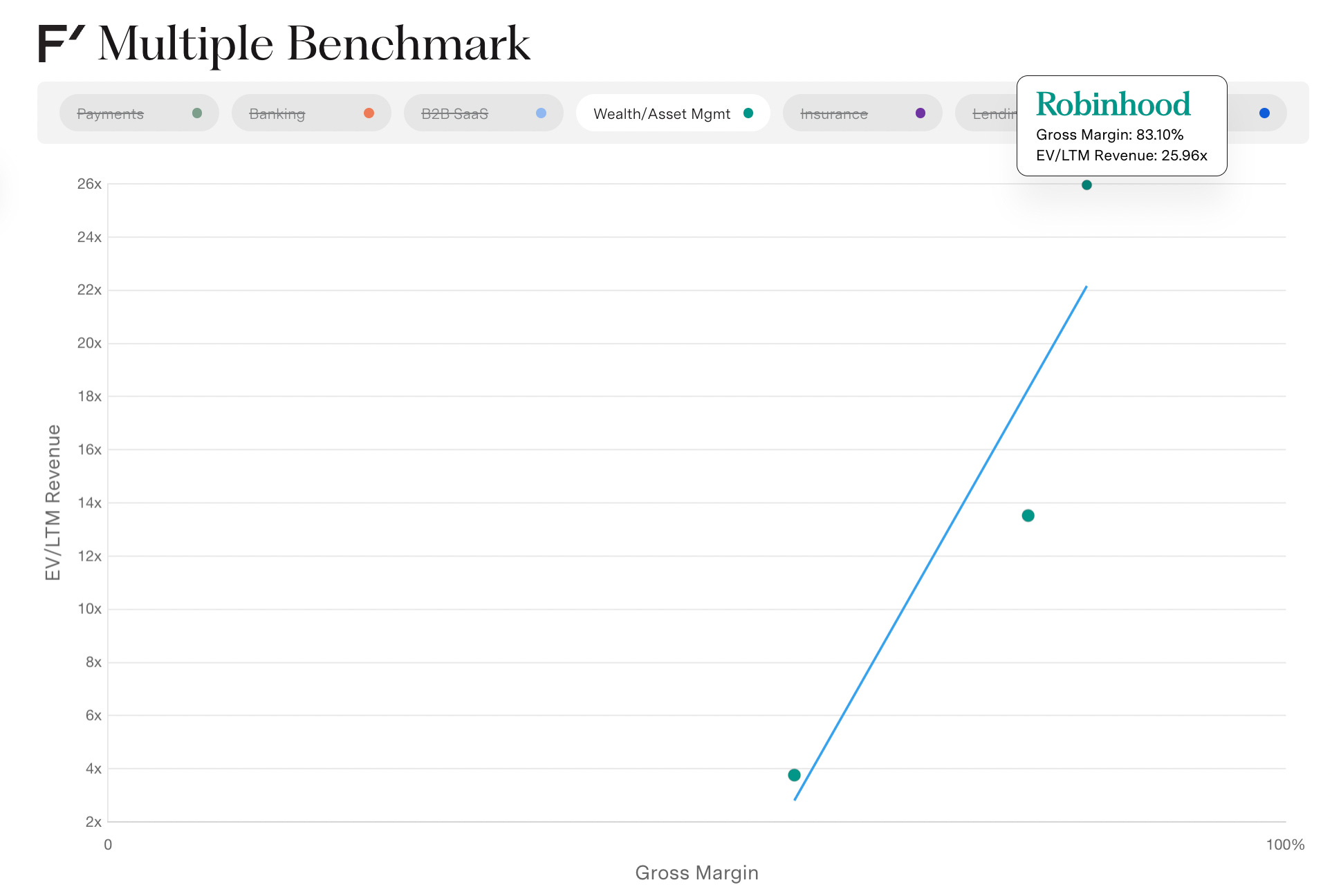

Performance was up meaningfully across the F-Prime Fintech Index in Q2 (+18.9 percent) with multiples rising from 4.4x last quarter to 5.6x, but the real story is in WAM, where public market multiples nearly tripled from 6.8x in Q1 to 18.6x. That’s the biggest single-quarter jump in recent memory. Digging deeper into the data, we find a 59.7 percent growth in LTM revenue for WAM companies, versus 25 percent for the overall F-Prime Fintech Index.

Two familiar names led the charge. One-time meme stock darling Robinhood has quietly staged a comeback, with its multiple shooting from 10.9x to 24.2x driven by a rebound in assets and trading volumes, with ~$100B in platform assets added over the past year (including $41B in RIA assets added in Q1), strong crypto activity, and expanding subscription products. The company is also posting very strong gross margins (83 percent), EBITDA margins (41 percent) while growing revenue 58 percent year-on-year. To further boost its stock prices Robinhood returned $322M to shareholders by repurchasing ~7M shares in Q1. This is the first time since Q1 2022 that we’ve seen a 24x multiple in the Fintech Index.

Meanwhile, Coinbase traded at a 12.9x revenue multiple, up from 6.3x last quarter. The crypto trading platform posted 76.4 percent LTM revenue growth, compared to 39 percent a year ago.

Meet The Fintech Index’s (Potential) Fresh Faces

There are only three WAM companies in the F-Prime Fintech Index right now (Coinbase, Robinhood, and Virtu Financial), but that’s about to change.

It has been three years since we’ve added any companies to the Index, but in Q2 we finally saw the drought break with a few IPOs and a SPAC merger. We typically wait 90 days for a company to season before we add it to the Index, but four companies — three WAM players and one banking company — are on track to join in Q3.

Webull (BULL) went public on April 11 via a SPAC merger on the Nasdaq stock exchange at a ~$7.3B valuation, though it now trades at a $6B market cap. Webull is a mobile-first brokerage platform known for its commission-free trading and active retail investor community. Its strength lies in catering to a younger, high-frequency trading audience with advanced charting tools and extended-hours trading.

eToro (ETOR) IPOed on the Nasdaq on May 14 at a $5.5B valuation. eToro is an Israeli social trading platform that lets users invest in stocks, crypto, and ETFs, and also allows users to copy the trades of other top investors. The company IPOed at $52 per share, closed Q2 at $66.59, and is now trading in the $55 range as we go to print.

Chime (CHYM) debuted on the Nasdaq on June 12 at $11.6B. Best-known as a neobank, Chime has expanded well beyond checking accounts. With products like fee-free overdrafts, credit-building tools, and early paycheck access, it’s increasingly moving into financial wellness territory, especially for underserved consumers. Chime priced its IPO at $27 per share, closed Q2 at $34.51 and is now trading around $30.

Stablecoin issuer Circle (CRCL) IPOed on the NYSE on June 5 and is already catching tailwinds from broader crypto resurgence. Circle is the company behind USDC, the second-largest stablecoin by market cap, and a foundational piece of crypto-financial infrastructure. As stablecoins move toward broader adoption, Circle is positioning itself at the intersection of payments, trading, and tokenized finance. The company IPOed at $31 per share, opened at $69 on its first day of trading and soared to $83 on the first day — 168% above its IPO price. Within weeks, the stock had spiked to nearly $300 per share, closed Q2 at $181 per share, and is now trading around $223 per share.

Look for some, if not all, those companies to appear in the F-Prime Fintech Index in Q3. Meanwhile, we’re also watching Klarna, which filed its S-1 back in March and could IPO by the fall, and ReserveOne, which is another SPAC in the works. Crypto asset manager Grayscale, blockchain-based lending and finance platform Figure Technologies, and digital bank Starling Bank have also filed (or are considering filing) to go public. Note that companies require at least 90 days of trading history and meet our criteria before we list them.

Finally, we also saw AvidXchange acquired by TPG and CPAY for $2.2B (a ~5x multiple on $441M LTM revenue) on May 6; and Redfin acquired by Rocket Companies for ~$1.75B (1.7x revenue on $1.04B LTM revenue) on July 1. Both have been removed from the F-Prime Fintech Index following the acquisitions. After quarter close, Olo entered into a definitive agreement to be acquired by PE firm Thoma Bravo in an $2B all-cash transaction (6.7x LTM revenue multiple on ~$300M TTM revenue). Olo will therefore be removed from the Index over the coming weeks.

Q2 Numbers

Fintech multiples snapped back across every growth tier in Q2. Companies with higher than 40 percent LTM growth traded at 4.5x, up from 3.1x in Q1. Companies at 20-40 percent LTM growth went from 6.3x in Q1 to 8.1x in Q2, and companies growing less than 20 percent ticked up slightly from 3.2x to 3.4x.

Across the board, LTM revenue growth itself has rebounded to an average of 25 percent, up from 17 percent a year ago. Median growth sat at 21 percent, only slightly down YoY (vs. 23 percent in Q2 2024).

As we noted above, WAM was in a league of its own in Q2, leaping from 6.8x to 18.6x revenue multiple. Elsewhere, we saw:

B2B SaaS grow from 7.5x to 8.2x

Lending grow from 5.1x to 5.9x

Banking grow from 4.1x to 4.9x

Payments grow from 4.2x to 4.9x

Proptech fall from 2.3x to 2.2x

Insurance grow from 1.6x to 1.9x

Keep an eye out for our new report on the State of Fintech: Wealth to be released next month.