Fintech in Q4: The Return of BNPL and (Maybe) Crypto

Plus State of Fintech buzz!

Welcome back to Fintech Prime Time, a monthly wrap of fintech industry data and analysis drawn from the F-Prime Fintech Index.

Our overview of fintech’s Q4 movements are but a taste of the big year-in-review we’re preparing right now: F-Prime Capital’s State of Fintech report. You can check out past reports on the F-Prime Fintech Index, and rest assured we will be in touch as soon as our 2024 edition goes live in early February.

For now, we invite you to join us when we present our findings in-person (well, on Zoom) on Tuesday, February 27 at 1 pm Eastern / 10 am Pacific. You can sign up here.

Okay, so what happened in fintech in Q4?

Unpacking Fintech’s Q4 Rise

By Abdul Abdirahman and Zoey Tang

Fintech as a whole rose in Q4. Before we jump into the numbers, it’s worth highlighting a few notable stories hidden within them:

The Return of Buy Now, Pay Later: In the 11 months ending December 6, consumers spent $64.9B via BNPL platforms — a 15 percent jump from a year earlier. The markets reflect that rise, with BNPL provider Affirm’s revenue multiples tripling since Q4 2022. The company now trades at 11.2x. We have not seen that level of persistence for a publicly listed digital lender before — after all, Affirm has moved beyond B2C point-of-sale lending. On that note, in November the company announced that its partnership with Amazon had expanded to cover payments on its B2B store. Meanwhile, a surge in BNPL usage over Black Friday and Cyber Monday (up 20 percent on Black Friday and 42 percent on Cyber Monday) also lifted the company’s earnings.

Fellow BNPL provider Klarna is one of the top candidates to go public in 2024. But keep an eye on regulators, as the OCC recently issued a bulletin to help banks manage the risks associated with BNPL. For a deeper analysis on the vertical from an unapologetic BNPL evangelist, we enjoyed Simon Taylor’s “rant” earlier this month.

Crypto Spring?: Coinbase is currently trading at 15.1x, up from 1.3x in the depths of the crypto winter. That’s a stronger bounce than we’ve seen in cryptocurrency prices — Bitcoin has rebounded from $16,529 in December 2022 to $42,800 this month and Ethereum is now worth $2,562, up from $993 in July 2022. $4.6 billion changed hands on the new bitcoin ETF’s first day of trading — though the price has corrected post-launch and Vanguard did not join the likes of BlackRock, Grayscale, and Fidelity in launching a spot bitcoin ETF.

Shopify’s on a Roll: The e-commerce platform’s multiples have increased again QoQ and now trades at double its Q4 2022 multiple at 14.5x. What’s driving this growth?

After pulling the plug on its logistics side quest in May, the company has re-focused on its main game: building e-commerce stores for brands, adding enterprise clients, facilitating better omnichannel and mobile commerce experiences, and building its wholesale offerings.

That wholesale business is gaining traction, with B2B GMV up 61 percent in the first half of 2023. New customers include Kraft Heinz, Brooklinen, and Momofuko.

Shopify has been well-placed to harness the tailwinds propelling vertical SaaS. Across the fintech category, investors consistently reward vertical SaaS companies over other fintechs for their recurring revenue, high gross margins, and economies of scale.

We’ll be exploring these themes and more in our State of Fintech report — remember to save your spot at our 2024 presentation here.

And now, for those of you who love diving into the details on public stocks, we have:

The Q4 Numbers

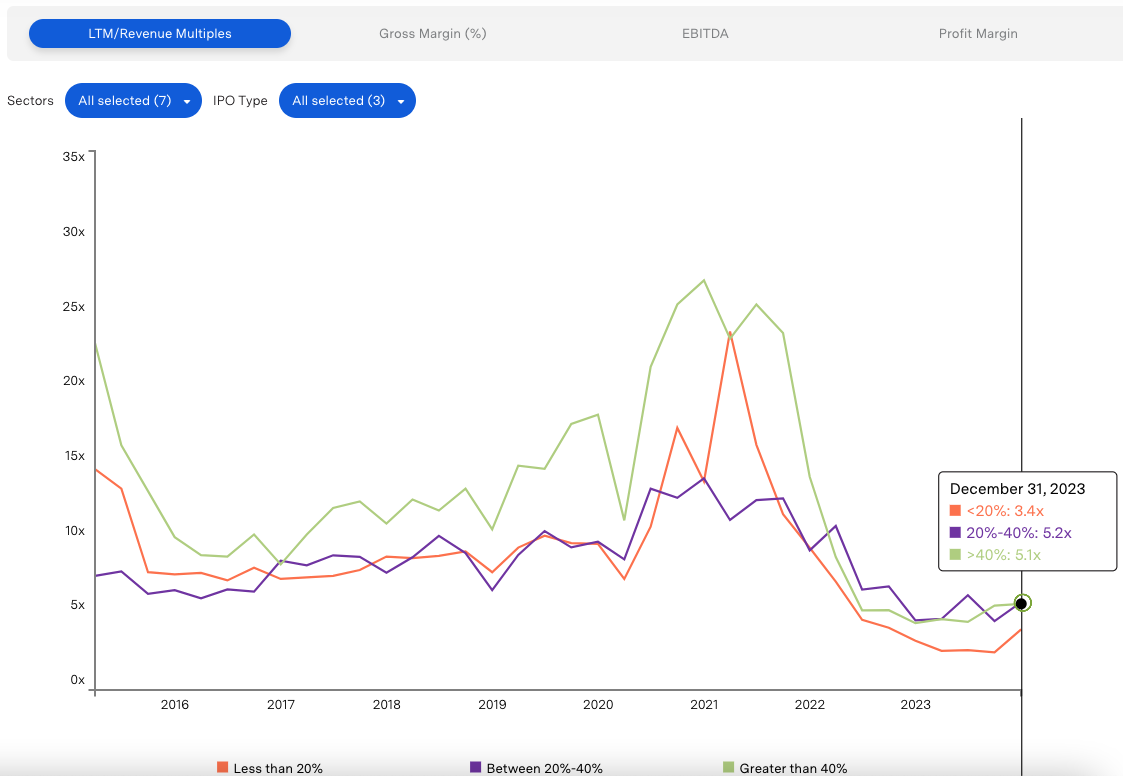

LTM revenue multiples rose across the board in the last quarter of 2023, from 4.0x in Q3 to 4.8x in Q4. Multiples rose for all growth rates and verticals within the sector.

By Growth Rate:

Companies that grew less than 20 percent (typically the larger companies in the Index) saw the biggest jump in Q4, almost doubling from 1.8x to 3.4x thanks to a broad recovery in market capitalization and enterprise value. The other two growth segments saw modest gains — find an interactive version of the chart above under “Historical Metrics” on the F-Prime Fintech Index.

By Vertical:

Wealth and asset management saw the largest jump, with average multiples rising from 3.4x to 7.3x. Coinbase and (to a lesser extent) Robinhood drove the rise — see below.

Proptech companies collectively traded above 1x for the first time since Q2 2022, rising from 0.9x to 1.5x. Digital mortgage platform Blend drove the rise for the second quarter in a row.

Zooming In on WAM

Driven by rising equity and crypto prices, WAM companies’ assets under management and transaction volume have rebounded. The overall crypto market capitalization is up 62 percent to $1.3T since the beginning of 2023. Since the WAM sector is mainly a tale of two companies, let’s check in on the main players individually:

Net quarterly revenue for Coinbase was down six percent in Q3 to $623M, but still higher than the $576M 12 months earlier. The company is marching towards profitability on a GAAP basis, only losing $2M in Q3 2023.

However, those aforementioned gains in the value of crypto assets and a corresponding rise in trading volume mean that Coinbase’s Q3 numbers were less than impressive in light of trade-based revenues. In the third quarter, Coinbase generated $289M worth of trading revenue (down 21 percent year-on-year), with $275M (95 percent) coming from consumer activity and another $14M (5 percent) from institutional traders. Those figures were $310M and $17M respectively in the second quarter of 2023, and $346M and $20M a year ago. For now, Coinbase’s main growth comes via interest-based income (including interest earned on customer custodial funds and loans), as well as subscriptions and services like its stable coin arrangement with Circle and USDC.

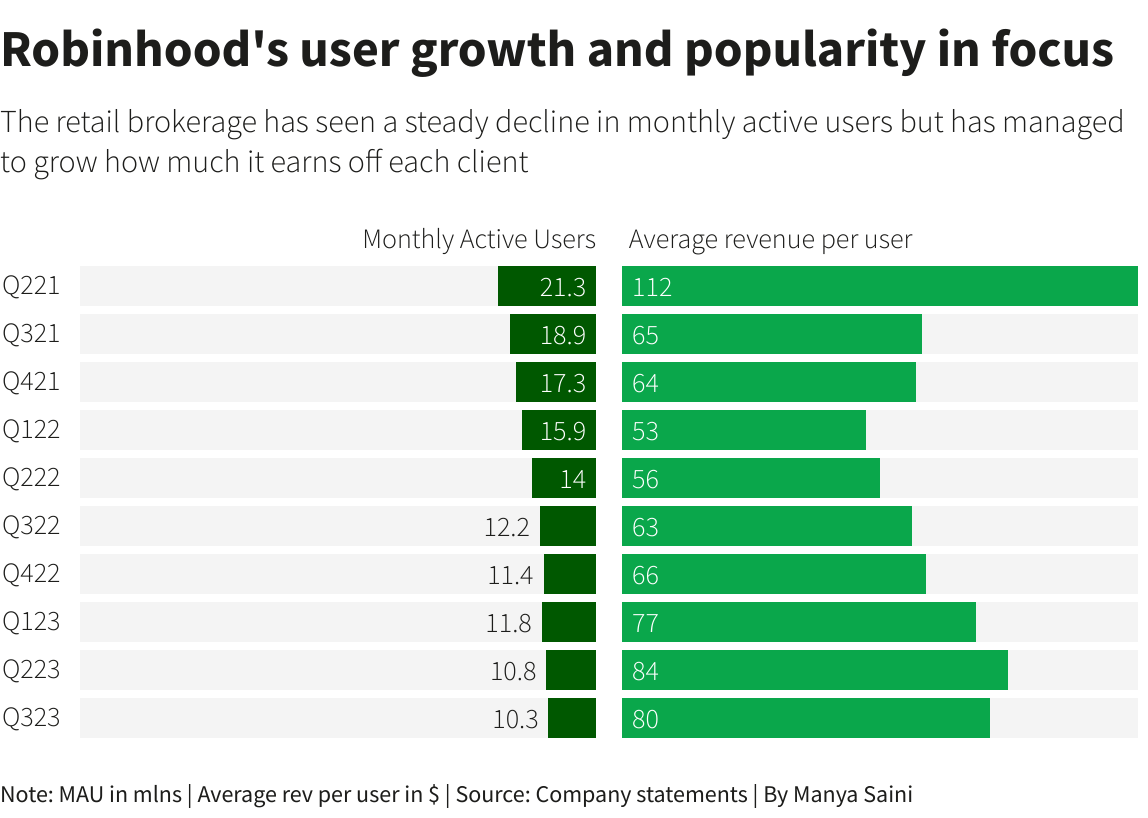

Monthly active users over at Robinhood have been declining month over month, but it has compensated somewhat with steady increases in its earnings per client over the last six quarters. Similar to Coinbase, it has also seen its revenue boosted by rising interest rates, with income from interest surpassing transaction-based revenue for the first time in the company’s history.

Index Removals: Finally, while M&A activity continues to pick up in both public and private markets, no F-Prime Fintech Index companies were acquired this quarter. However, crypto trading platform Bakkt no longer met our criteria and was removed from the Index.